Thesis

By the end of 2021, approximately 1.4 billion adults globally remained unbanked. Although the COVID-19 pandemic accelerated the number of banked people worldwide, the Global Findex Database estimates that only 76% of the populace owned an account with a financial institution. These individuals remain unbanked for various reasons, primarily citing minimum balance requirements and general distrust of banks. Low-income individuals face high barriers to entry with traditional banks, such as minimum opening deposits ranging from $25-$100, varying minimum monthly deposits, monthly service fees averaging $16.19, and overdraft fees averaging $29.80. Additionally, these unbanked individuals are commonly difficult-to-reach demographics, unable to easily access retail banking locations.

Neobanks, or ‘challenger banks’, are fintech firms specializing in mobile and online banking that seek to challenge the status quo of traditional banks. These alternative financial institutions build solutions to address the issues relevant to the global unbanked/underbanked populace. The advent of neobanks was primarily driven by consumer skepticism of traditional financial institutions following the 2008 global financial crisis. Since the first neobanks began operations in the early 2010s, consumer demand for these services rapidly grew, evidenced by the approximately 400 institutions operating globally as of 2022.

Neobanks can reduce overhead costs by offering online-first services, eliminating the need for physical locations. This expense reduction can enable neobanks to offer fee-free accounts to underbanked demographics. Further, online-first financial institutions can address the needs of difficult-to-reach demographics, such as individuals in rural communities physically distanced from retail locations. Global consumer adoption of fintech reached 64% in 2019, up from 15% in 2015. The main driving force behind this growth was the more attractive rates and fees offered by fintech companies in comparison to traditional financial institutions.

Revolut is a London, UK-based neobank that initially offered money transfer and exchange services to reduce the costs of international exchange rates charged by traditional banks. Since launching in 2015, Revolut has expanded to offer additional financial services, such as automated investing, corporate banking, spending rewards, international transfers, multi-currency accounts, and travel insurance. Revolut established itself as one of the largest neobanks by account holders in the UK and Europe. In 2020, the company expanded operations to the United States and announced plans to expand to Latin America, Asia, and the Middle East in the upcoming years.

Founding Story

Revolut was founded in 2015 by Nikolay Storonsky (CEO) and Vlad Yatsenko (CTO). Storonsky was born in Russia, where he graduated with a Master's in Applied Economics and Finance, as well as a Master's in General and Applied Physics. Yatsenko was born in Kyiv, Ukraine, and graduated in 2006 from the National University of Kyiv-Mohyla Academy with a Master's in Computer Science.

Storonsky began his career in 2006 as an equity derivatives trader at Lehman Brothers. In 2008, he left Lehman to work at Credit Suisse in the same role. In June 2013, Storonsky left his job at Credit Suisse and in January 2014, started working on Revolut. Yatsenko's career began in 2005 as a software engineer at Nibulon Ltd. After several years as a software engineer at different companies, Yatsenko entered the finance sector as a Senior Developer at UBS Investment Bank. He later worked at Deutsche Bank, Lab49, and Credit Suisse, where he worked on an equity derivatives risk platform.

Storonsky's experience at Lehman shaped what Revolut is today. During the 2008 housing crisis, when Lehman went bankrupt, Storonsky lost around $690K and learned an important lesson: "Back up decision-making with data and logic." Storonsky came up with the initial idea for Revolut when traveling abroad, where he became frustrated with the high fees and poor exchange rates that traditional banks charged. As a result, Storonsky teamed up with Yatsenko to create a prepaid debit card that would enable users to spend multiple currencies at the interbank exchange rate.

Revolut’s mission is “to simplify all things money.” The founders' experience in the financial sector allowed them to understand that to make a business out of Revolut, they needed to eliminate as many middlemen as possible and build infrastructure in-house. In 2019, the company attracted significant attention due to allegations of a toxic work environment and claims that the company had turned off compliance checks systems, resulting in an FCA probe. Since then, the company has brought industry veterans such as Martin Gilbert (co-founder & CEO of Aberdeen Asset Management from 1983-2017) as chairman, Michael Sherwood (former Co-Chief Executive at Goldman Sachs International), and Ian Wilson (previously an executive at RBS, Santander, Tesco Bank, Charter Court Financial Services, and Monzo) as Non-Executive Directors on board, and hired a new PR team to regain public trust.

Product

Personal Banking

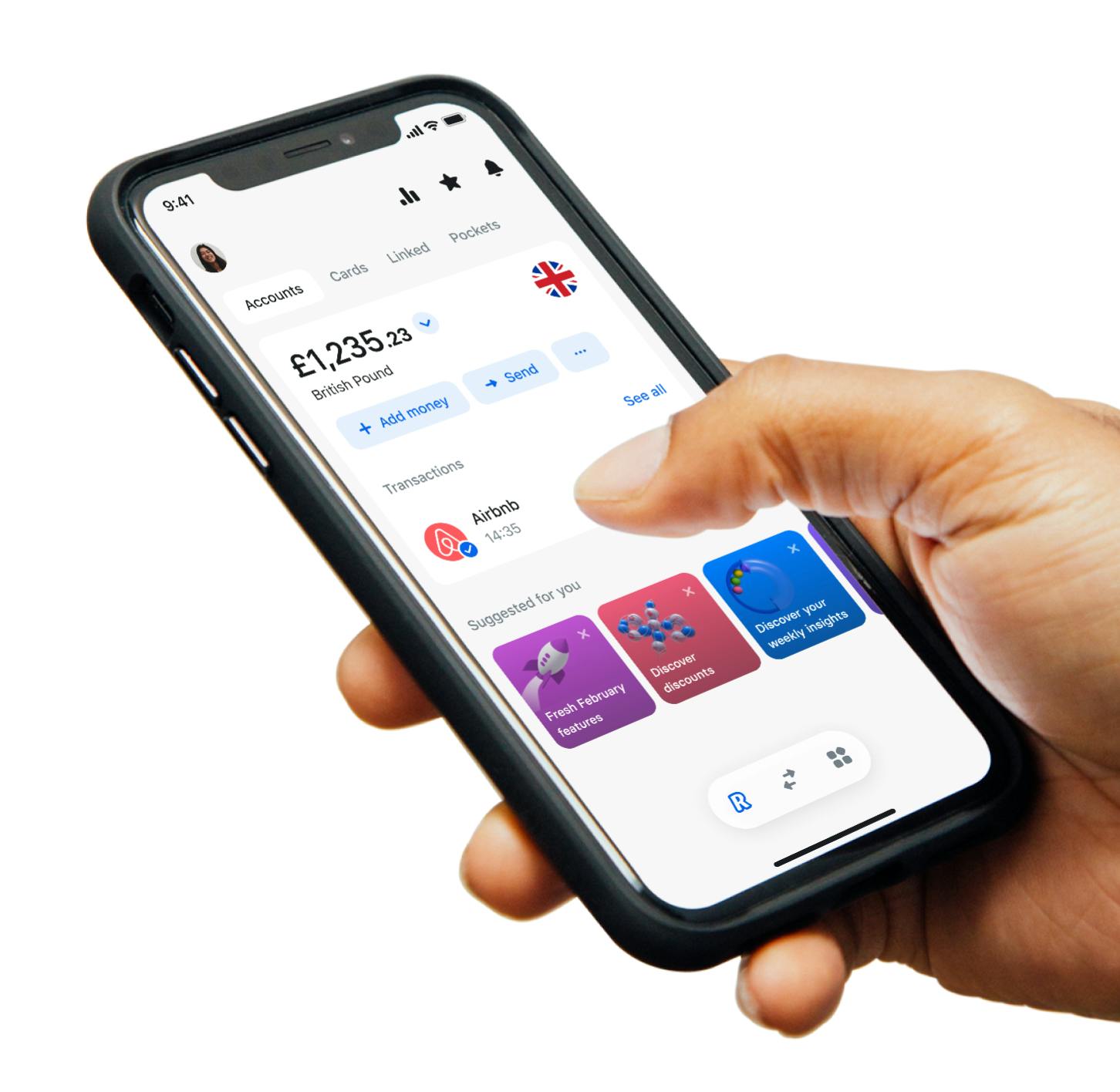

Revolut is a digital banking app that provides financial service solutions. Users can send, spend, and invest money in stocks and cryptocurrencies through the app. The app also enables users to manage their subscriptions, simplifying and enhancing their financial management. The product is divided into three main areas: Essentials, Wealth, and Lifestyle.

Essentials: Revolut's Essentials enables users to transfer money, make payments, and split bills, with users spread across more than 200 countries. It also offers a currency converter, enabling users to purchase and hold up to 29 fiat currencies and over 100 crypto tokens. The app provides instant payment notifications and in-app card security management. Revolut also offers several services as part of the Essentials package including:

Early Salary enables users to request and receive their salary a day earlier without fees.

Rewards provide users with discounts and cash back at selected stores.

Saving Vaults allow users to earn up to 3% AER/Gross (variable) paid daily.

Open Banking provides a dashboard for users to view bank accounts from multiple providers in a single interface within the Revolut app.

Subscription Management enables users to oversee subscriptions, receive trial notifications, and block subscription charges.

Wealth: Revolut offers various investment vehicles on its platform for customers to trade and purchase, including rare metals (e.g., gold, silver), stocks, and cryptocurrencies. Users can start investing in over 1.5K global shares commission-free, starting with $1. The company provides real-time updates and notifications regarding held securities. Additionally, Revolut provides educational materials and courses to educate users on investing in stocks and cryptocurrencies. The app allows users to set price alerts on cryptocurrencies to buy and sell and to improve awareness. Cryptocurrencies purchased and traded on the platform are stored in cold storage and can be used directly from the customer’s physical card. The platform features an in-app commodities investing tool for buying and selling gold, silver, and other metals.

Lifestyle: Revolut users can book holiday accommodations within the platform, earning up to 10% cash back on purchases. While traveling, customers can access over 1K airport lounges for additional costs. Further, customers can spend money at real exchange rates in 29 currencies while traveling without hidden fees. Users can send gifts through the app to other Revolut users and donate money to charities without fees. Additionally, Revolut offers pet insurance and 24/7 vet access via video call for additional costs.

Source: Revolut

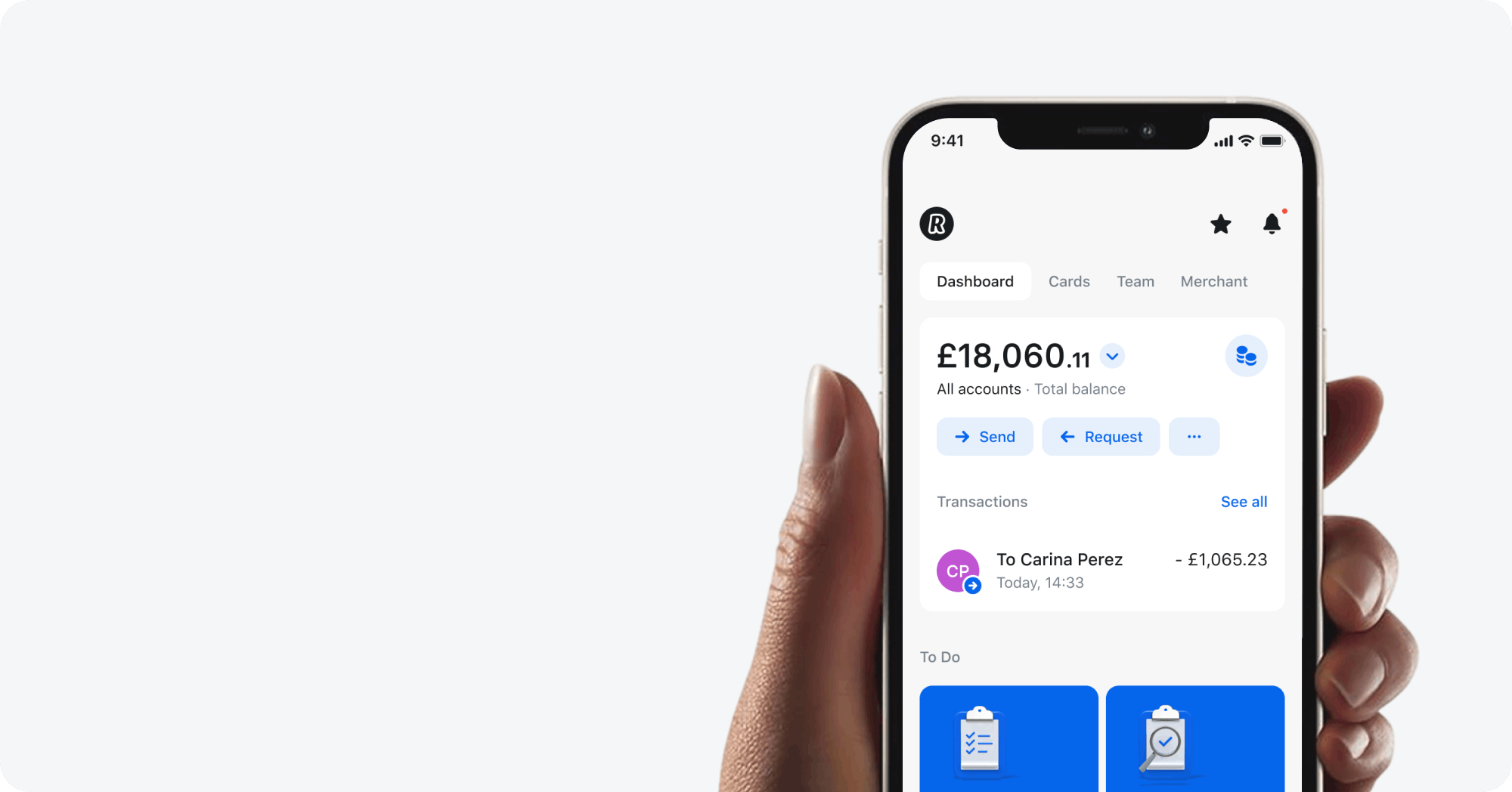

Business Banking

In addition to offering financial services for consumers, Revolut offers parallel business products. The company’s business banking platform is similar to the product areas of personal banking but with added tools and analytics. These enhancements help businesses send and receive money from anywhere in the world in over 25 currencies.

Essentials: Businesses can invite team members to their accounts and manage spending in real-time. Customers can also send money globally and set up multi-currency accounts in over 25 currencies. Spend Management allows businesses to automate their bookkeeping process by integrating with Xero, QuickBooks, or Sage. Managers can issue physical and virtual cards to team members and can control spending by setting limits, freezing cards, and automatically reminding staff to submit expense receipts.

Treasury: Clients can engage in 24/7 foreign exchange (FX) trading from Revolut’s web and mobile applications with real rate exchange, limit/stop orders, and price alerts. Businesses can also make forward exchange contracts to lock in future exchange rates. Additionally, Revolut enables customers to trade cryptocurrencies to diversify cash holdings.

Payments: This feature enables clients to accept payments in multiple currencies through Revolut’s payment gateway API, payment links, QR codes, Revolut Reader (the company’s point-of-sale card reader), and Revolut Pay. The company’s payment gateway and link solutions facilitate online checkouts, and funds are available the next day. In November 2021, Revolut acquired Nobly POS to expand into online and offline payment processing for the hospitality sector. Nobly POS is the ePOS that is integrated into Revolut Reader.

Tools: Revolut provides teams with a dashboard to manage, plan, and track their spending. The company offers invoicing software and payroll management to set up employee pay. Its business banking solution also features a rewards program that provides discounts and credits on business tools. With physical and virtual debit cards, managers can control spending and permissions within a single interface while automating expense tracking by utilizing instant reminders for team members to upload receipts.

APIs: The business banking solution allows clients to access their API, customize their online payment experience, or automate payouts. Businesses can connect their own applications to receive payments from customers. Users can also integrate the Revolut API to automate payments to suppliers and other service providers, create requests to access data from their account, view all transactions and generate reports, use webhooks to receive instant updates, and request user data with OAuth.

Source: Revolut

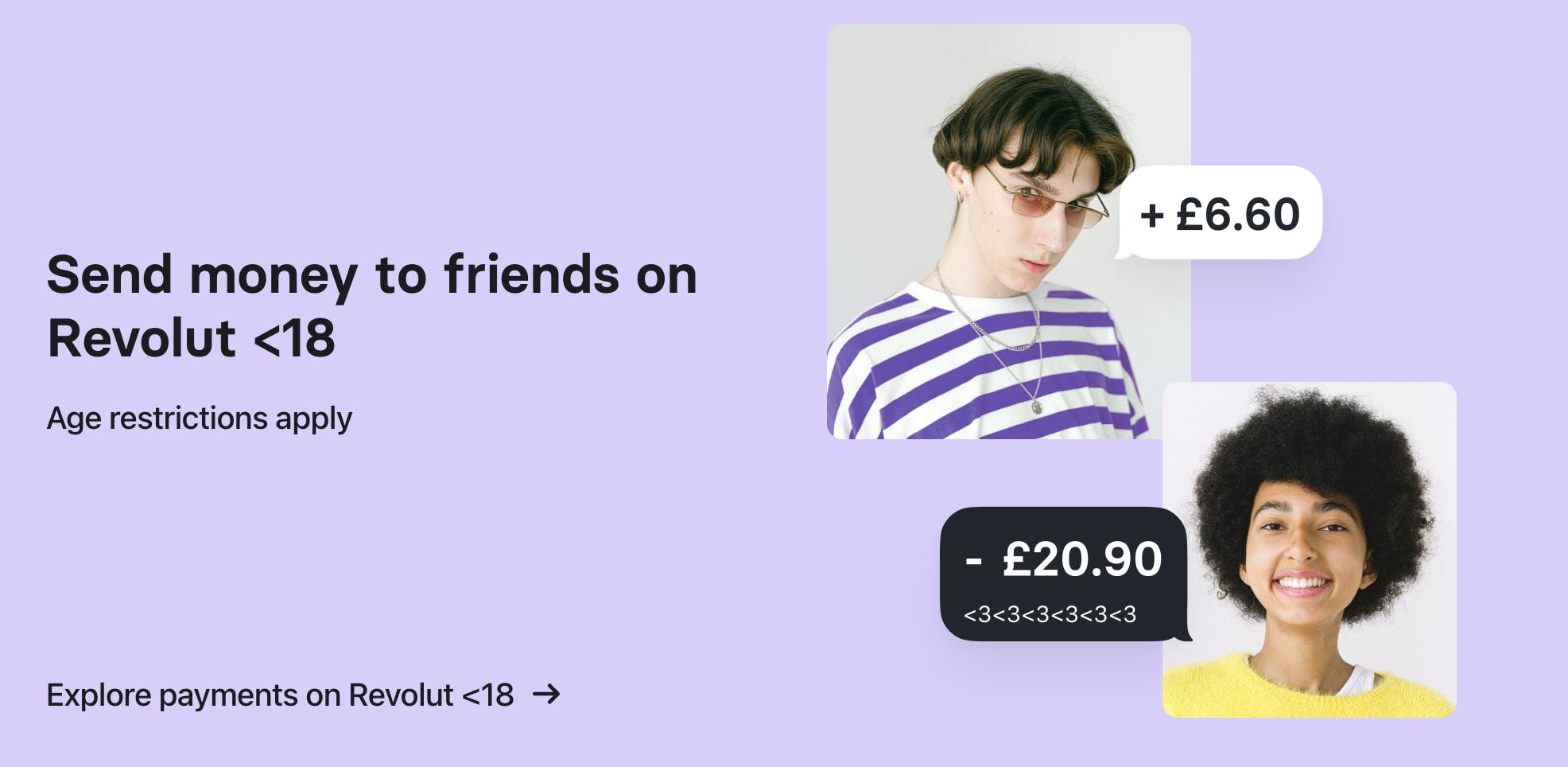

Revolut <18

Revolut <18 is the company's banking service built for individuals aged 6 to 17. This service allows these users to spend, send, and save money. It also provides features for setting financial goals. This service includes a customizable, contactless physical card featuring various designs. Parents/guardians can set up tasks and challenges for teens to earn money.

Source: Revolut

Market

Customer

Revolut offers products for personal banking, businesses, and freelancers. As of June 2023, Revolut operates in countries of the European Economic Area, Australia, Singapore, Switzerland, Japan, the United Kingdom, and the United States. The company’s products target digital users seeking a comprehensive solution for spending, saving, investing, traveling, and financial management. In the retail customer base, Revolut targets frequent international travelers seeking to reduce currency exchange fees.

As of June 2023, Revolut surpassed 30 million global retail customers. The company’s largest geographical retail customer base is the United Kingdom (6.8 million), followed by Romania (2.8 million) and Poland (2.5 million). Revolut’s B2B products are primarily targeted at globally operating businesses due to the international capabilities and foreign currency exchange. The company notes use cases for internationally-scaled companies such as SaaS, travel, e-commerce, and online marketers. Before Revolut, these internationally-scaled businesses relied on multiple service providers, such as traditional banks, brokers, insurance companies, travel agencies, and local exchange houses. Revolut, however, offers all these services on its platform. Some of Revolut’s business clients include Deel, Creditspring, Bizaway, and Dott.

Market Size

Revolut is a fintech company competing in the neobank sub-sector. At the end of 2021, approximately 76% of the global population held an account with a financial institution. In 2022, neobanks held approximately 1 billion global accounts. According to research published in 2022, the international neobanking market has a total value of $66.8 billion, growing at a projected 58% CAGR from 2023 to 2030 to reach $2.8 trillion. This market is inclusive of both retail and business banking services, both of which are offered by Revolut. 29% of the global revenue of neobanks came from Europe, Revolut's largest market. The fastest-growing market for the neobank industry is Asia, evidenced by the approximately 70% of adults who are currently unbanked or underbanked in Southeast Asia as of 2022.

Competition

N26: Founded in 2013, N26 is a mobile-only banking app for users in the EU. The neobank offers both personal and business banking, each with dedicated plans for different types of users. The personal banking plans start from the standard free account and go up to the metal plan, which costs €16.90 a month and includes perks such as travel and mobile phone insurance. The business banking plans, targeted towards small freelancers and large companies alike, have the same price range and plans as personal banking.

Through the N26 app, users can send, receive, and pay through physical or virtual cards. There are no transaction fees for payments in different currencies. Its product also offers travel insurance, a crypto exchange, cash back, phone coverage, and analytics. N26 is available in 22 countries across the EU. N26 raised a $900 million Series E round of funding at a $9 billion valuation in 2021. Overall, the company has received over $1.7 billion in funding. In 2021, N26 reported around $200 million in revenue and a net loss of around $190 million. In 2021, the company gained 1 million customers, bringing its total user base to 8 million.

Monzo: Founded in 2015, Monzo is a digital bank based in the UK that is expanding into the US. Backed by Y-Combinator, Monzo has over 8 million users and offers personal and business banking and borrowing services. Accounts for personal banking start for free and go up to £15 per month. Paid plans include travel insurance, phone insurance, saving accounts, discounted airport lounge access, and credit scoring. With Monzo Flex, users can buy-now-pay-later, allowing users to purchase in three monthly installments interest-free or 6-12 installments with interest. Revolut does not offer an alternative to Monzo Flex.

As of May 2023, Monzo had over 7.4 million users. In 2021, Monzo generated £79 million in revenue and grew to £154.2 million in 2022. The company raised a $500 million Series H in 2021 at a $4.5 billion valuation from investors including Tencent Holding, Abu Dhabi Fund, Accel, and General Catalyst.

Starling Bank: Founded in 2014, Starling Bank is a digital banking solution for UK citizens that offers personal banking accounts for individuals, joint accounts, accounts for teens, business banking, overdraft protection, and loans. Personal accounts offer users physical and virtual cards, lending, bill management, and zero fees for spending and withdrawing money abroad. Starling Bank targets UK individuals and businesses with multi-currency accounts such as EUR, USD, and GBP. Accounts on Starling Bank can also send money transfers to bank accounts in 36 countries. All personal and business bank accounts are free of charge. Starling Bank monetizes by charging a foreign exchange transfer fee of 0.4% and its loan-provider services.

In March 2022, the company reported that it had over 2.7 million customer accounts; this same year, Starling Bank achieved profitability of £32.1 million. As of June 2023, the company had over 3 million accounts. The company raised an internal funding round of £130.5 million, which gave the company an approximate £2.5 billion valuation. In 2021, Starling Bank raised £322 million of Series D funding, which included investors such as Goldman Sachs, Fidelity, and Qatar Investment Authority.

Monese: Launched in 2015, Monese was the first mobile bank in the UK. Now available in countries throughout the EU, the company offers personal and business banking. For personal banking, the company offers three plans starting from its free Simple plan to a £14.95 a month Premium plan. In its personal banking accounts, users can set up multi-currency accounts, send money, pay in various currencies, and manage budgets. For business banking, Monese offers one plan with a price tag of £9.95 a month, giving companies personal accounts, debit cards, foreign currency payments with a 0.5% fee per transaction, and foreign currency transactions with a 0.5% fee per transaction to non-Monese accounts. In 2022, the company secured $35 million from HSBC, bringing its total funding to $208 million.

Chime: Chime is the largest US neobank by account holders, with over 21.5 million accounts as of January 2023. Chime currently operates in the US and offers customers both checking and savings accounts without monthly fees. Chime also offers customers a credit builder product which helps clients build a healthy credit history. In 2022, Chime delayed its IPO, which had a targeted valuation of $35 billion to $45 billion. As of June 2023, Chime has received a total of $2.3 billion in funding. The company raised $750 million Series G in August 2021, which put the company at a $25 billion valuation.

Business Model

Revolut offers its banking service for free by building in-house infrastructure and eliminating costs such as the fixed costs of maintaining physical branches. To support the free service, it sells add-on services to users. To monetize, Revolut needs to maintain a large user base to cross-sell these services. As of June 2023, Revolut offers five personal banking plans ranging from free to £45 a month, four business banking plans ranging from free to £100 a month with custom pricing for enterprises, and three freelancer plans ranging from free to £25 a month. The company also monetizes via transaction fees on its payment product.

Personal Banking Plans

Standard Free: Revolut’s Standard Free plan includes a physical card and offers free ATM withdrawals up to £200 or five monthly withdrawals and £1K fee-free monthly currency exchange. Additionally, the company offers up to 3% cash back on accommodations, up to 2.29% AER/Gross (variable) interest on savings, 1.49% crypto exchange fee, and 1.99% exchange fees.

Plus: Revolut Plus, priced at £2.99 a month, includes all features from the Standard Free plan plus a personalized card, in-app chat support, and up to 2.39% AER/Gross (variable) interest on savings.

Premium: Revolut Premium, priced £6.99 a month, includes a 20% discount on international transfer fees, £400 of fee-free monthly ATM withdrawals, everyday insurance, discounted airport lounge access, unlimited fee-free currency exchange, up to 5% cash back on accommodations, £10 million on global medical insurance, £3K a year winter sports insurance, £1K a year luggage insurance, up to 3% AER/Gross (variable) interest on savings, 0.99% crypto exchange fees, and 1.49% commodity exchange fees.

Metal: Revolut Metal, priced at £12.99 a month, provides users with a personalized metallic card, 1% cash back on card payments, a 40% discount on international transfer fees, £800 fee-free monthly ATM withdrawals, up to 10% cash back on accommodations, £2K a year limit on car hire excess insurance, £1 million a year personal liability insurance, up to 3.44% AER/Gross (variable) interest on savings, and all other services provided in the Premium plan.

Ultra: Revolut Ultra, priced at £45 a month, includes a platinum-plated card, in-app chat or support calls, free international transfer fees, £2K fee-free monthly ATM withdrawals, partner subscriptions such as WeWork, unlimited airport lounge access, trip cancellation insurance, and all other services provided in the Metal plan.

Business Banking Plans

Free: Revolut’s Free plan for businesses offers clients up to three plastic cards per team member, up to 200 virtual cards per team member, five fee-free local payments, a 1.99% fee on crypto transactions, the ability to spend in 150 countries and hold over 25 currencies, free transfers to Revolut accounts, international bank account numbers (IBANs) for global transfers, the ability to accept online payments, invoice creation, and team spend management.

Grow: Revolut’s Grow plan, priced at £25 a month, offers clients 100 fee-free local transfers and 10 fee-free international transfers per month, £10K in foreign currency exchange at the real exchange rate, and a 0.99% fee on crypto transactions. It also includes all the features from the Free plan, analytics, rewards, API integrations, limit and stop orders, connection with bookkeeping apps, and Revolut Payments for accepting online and in-person payments.

Scale: Revolut Scale, priced at £100 a month, is designed for larger businesses and offers two metal cards, 1K fee-free local transfers, 50 fee-free international transfers per month, £50K in foreign currency exchange at the real exchange rate, and all features included in the Grow plan.

Enterprise: Designed for large businesses, the Revolut Enterprise plan is customizable and negotiable for pricing and features. Clients can negotiate with the Revolut sales team to customize a plan different from Revolut’s three traditional options.

Freelancer Banking Plans

Freelancer Free: Revolut’s Free plan for freelancers comes with five fee-free local transfers per month, a free physical card, access to over 25 currencies, an expense management tool to track business expenses, free transfers to Revolut accounts, IBANs for global transfers, the ability to accept online payments, invoice creation, and team spend management.

Professional: Revolut Professional, priced at £7 a month, offers 20 fee-free local transfers and five free international transfers per month, and £5K in foreign currency exchange at the real exchange rate. It also includes all the features from the Freelancer Free plan, plus analytics, rewards, API integrations, and limit/stop orders.

Ultimate: Revolut’s Ultimate plan, priced at £25 a month, includes everything in the Professional plan plus one free metal card, 100 fee-free local transfers and 10 free international transfers per month, £10K in foreign currency exchange at the real exchange rate, and discounted payment fees.

Payment Acceptance

Revolut Pay enables businesses to accept payments in over 25 currencies. Revolut offers business payment acceptance services for online and in-person checkout. For online payments, businesses are charged starting from 0.8% plus £0.20. Transaction fees vary depending on the type of card and country of origin of the card, with European consumer cards charged at 1% plus €0.20 when a client pays with a UK consumer card and 2.8% plus £0.20 for international and commercial cards. For in-person transactions, businesses are charged 0.8% plus £0.02 for UK cards and 2.6% plus £0.02 for international cards.

Traction

Founded in 2015, Revolut gained over 100K personal banking users in its first year. In 2019, the company reached over 10 million customers, and by 2020 grew to 14.5 million. As of June 2023, Revolut reported having over 30 million personal users and over 500K business users, with over 10K new businesses joining monthly and over 130K business cards issued monthly.

In 2021, Revolut generated $769 million in revenue, with a net income of $31 million and a 70% gross margin. Foreign exchange and wealth services accounted for 55% of the revenue generated. The same year, the company raised an $800 million Series E funding round at a $33 billion valuation, resulting in a 42.9x revenue multiple.

Valuation

Revolut’s latest funding round was an $800 million Series E in July 2021, valuing the company at $33 billion. This round included top investors like Tiger Global and SoftBank Vision Fund. As of June 2023, the company has reportedly raised total funding of $1.7 billion. In 2017, the company initiated a crowdfunding campaign and raised $5.3 million in just 24 hours.

Key Opportunities

Lending

Revolut could consider expanding its service offerings and providing clients with micro-loans or cash advances at low interest rates. By utilizing its current client data and Open Banking, Revolut could potentially develop accurate credit scores to mitigate default risks. Personal loans and mortgages are an opportunity that Revolut’s UK-based competitors, Monzo and Starling Bank, are pursuing.

For example, Monzo offers users lending through personal loans and buy-now-pay-later products. These products had a 193% YoY change from 2022 to 2023, amounting to a total value of £790 million. Lending interest income for Monzo is £90 million in 2023, which is around 47% of its total income. On the other hand, Starling Bank offers mortgage loans to users and has a total lending portfolio of £4.9 billion, of which around 70% are mortgage loans (£3.4 billion) as of 2023. For Starling Bank, interest income composes 81% of its total income in 2023 (£364 million), making lending its most powerful product offering.

Global Expansion

Globally, there are 1.4 billion adults outside of the financial system as of 2022, most of whom come from developing regions such as Asia, Africa, and Latin America. Revolut offers international money transfers, and this service can be leveraged to reach new markets where the number of unbanked adults is greater. By expanding to developing regions, Revolut could grow its user base and increase the number of serviceable markets to sell its other product offerings.

In 2022, the company began to pursue new markets, making key hires globally, including Glauber Mota as CEO of Revolut Brazil, Paroma Chatterjee as CEO of Revolut India, and Juan Miguel Guerra as CEO of Revolut Mexico. Revolut plans to launch in Brazil, India, Australia, and New Zealand in 2023. Today, users in Latin America can sign up for a waiting list. The new hires and expansion to new markets indicate that Revolut is betting on global expansion to developing regions, such as Asia, Latin America, and the Middle East. Over 350 million African citizens are outside the financial system, representing another potential future market expansion.

AI and Machine Learning

In 2019, a Telegraph article reported on Revolut’s controversial sanctions screening system detection system suddenly shutting down, prompting the FCA to investigate the matter. By investing in machine learning and AI money-laundering detection systems, the company can develop new ways to comply with regulators. Moreover, investing in these technologies could allow Revolut to expand its product through personalized financial advice and enhance customer engagement and user experience.

Key Risks

Competition

Neobanks face considerable competition, both from traditional financial institutions and other neobanks. Revolut must continually expand and differentiate its product offering to remain a market leader. However, this might cause issues in terms of cost and company operations, limiting potential growth. Traditional banks threaten neobanks because they have large consumer bases and can build spin-off products that directly compete with neobanking products, such as Santander Bank’s Open Bank. Traditional financial institutions can leverage years of experience in the financial sector. Additionally, as of August 2023, there are nearly 400 global neobanks. Revolut could struggle to differentiate from products offered by competing neobanks to remain a market leader.

Business Model Risk

Revolut’s business model heavily relies on selling low-margin vertical product offerings such as travel insurance and asset trading. In the long term, neobanks have been the subject of discussion about whether or not they can achieve profitability. In 2022, Christoph Stegmeier, a senior partner at Simon-Kucher’s global banking practice, noted that only 5% of neobanks are profitable. Selling products such as travel insurance and currency exchange are at risk of potential economic downturns due to changes in consumer behavior.

Expansion Limitation

Expansion to newer markets to acquire new users is crucial to Revolut’s business model. In 2019, Storonsky, the CEO and founder of Revolut, noted that the company’s priority was global expansion and that becoming profitable was not its current focus. However, since 2019, the company hasn't expanded its global plan to countries outside the EU and the US. Now, developing markets like Latin America are dominated by regional fintech companies such as Nubank. The presence of competing neobanks in regional markets could create friction in Revolut’s global expansion path. This slow pace of expansion into developing markets could potentially limit Revolut’s global reach, thereby limiting its potential growth.

Summary

Revolut, a UK neobank founded in 2015, operates in the EU, the UK, and the US. The neobank challenges traditional banking models by offering digitized infrastructure, global reach, simplified foreign currency exchange, and affordable services. It provides personal and business banking solutions and provides multiple vertical services. Since its founding, Revolut has experienced substantial growth, with over 30 million personal users and 500K business users as of June 2023. Despite compliance issues, the company has taken steps to regain public trust. In 2021, the company generated revenue of $769 million and has raised $800 million in funding at a valuation of $33 billion.